Understanding the Market Impact of Another War in the Middle East

Many of our recent communications have focused on how investors should navigate uncertainty and volatility in the markets.

Unfortunately, the current environment continues to offer no shortage of both.

The latest escalation in the Middle East is yet another example of how quickly geopolitical (and political) events can unsettle markets and test investor discipline. Today we’re absorbing the impact of military strikes, retaliatory attacks, threats of wider escalation, disruptions to oil production and shipping, and rapidly rising energy prices. These are the dominant themes across financial news and everyday media, which means investors are naturally trying to determine what the potential economic consequences could be.

Trying to trade markets based on rapidly changing headlines is among the most hazardous strategies investors can pursue. Geopolitical events rarely follow predictable timelines, and early reporting during periods of conflict is often incomplete or contradictory.

In our view, the right question from an investment standpoint is not simply how long the conflict might persist. The more relevant issue is whether it meaningfully alters the economic backdrop through identifiable channels such as energy supply, inflation, corporate profitability, or global financial conditions.

History is often the right place to go searching for answers, in my view.

When Iraq invaded Kuwait in August 1990, triggering the Gulf War, markets initially reacted sharply. Oil prices surged and stocks declined as investors feared a wider conflict and severe disruption to energy supplies. Yet once the scope of the conflict became clearer and military operations progressed, markets stabilized. The U.S. economy entered the early 1990s recovery shortly thereafter, and equities rallied nearly +100% in the three years following initial strikes.

A similar pattern unfolded during the Iraq War in 2003. Kari and I were only a couple of years into building RSMA Wealth Management at that point, having just navigated the tech bubble. Those early years reinforced something that has shaped our investment philosophy ever since: our job is not to predict geopolitical outcomes, but to keep portfolios aligned with the economic forces that ultimately drive markets over time. 2003 turned out to be the first year in a long bull market, even as fighting broke out in that multi-year war.

I understand that today’s war feels different, for a host of reasons. The end game is unclear, and the potential closure of the Strait of Hormuz represents a risk the world has not meaningfully confronted since the late stages of the Iran-Iraq War in the 1980s. 20 million barrels of oil per day—about 20% of global supply—passes through the Strait. If shipments through that corridor were significantly disrupted for an extended period, it could have implications for oil prices, inflation, and global economic activity.

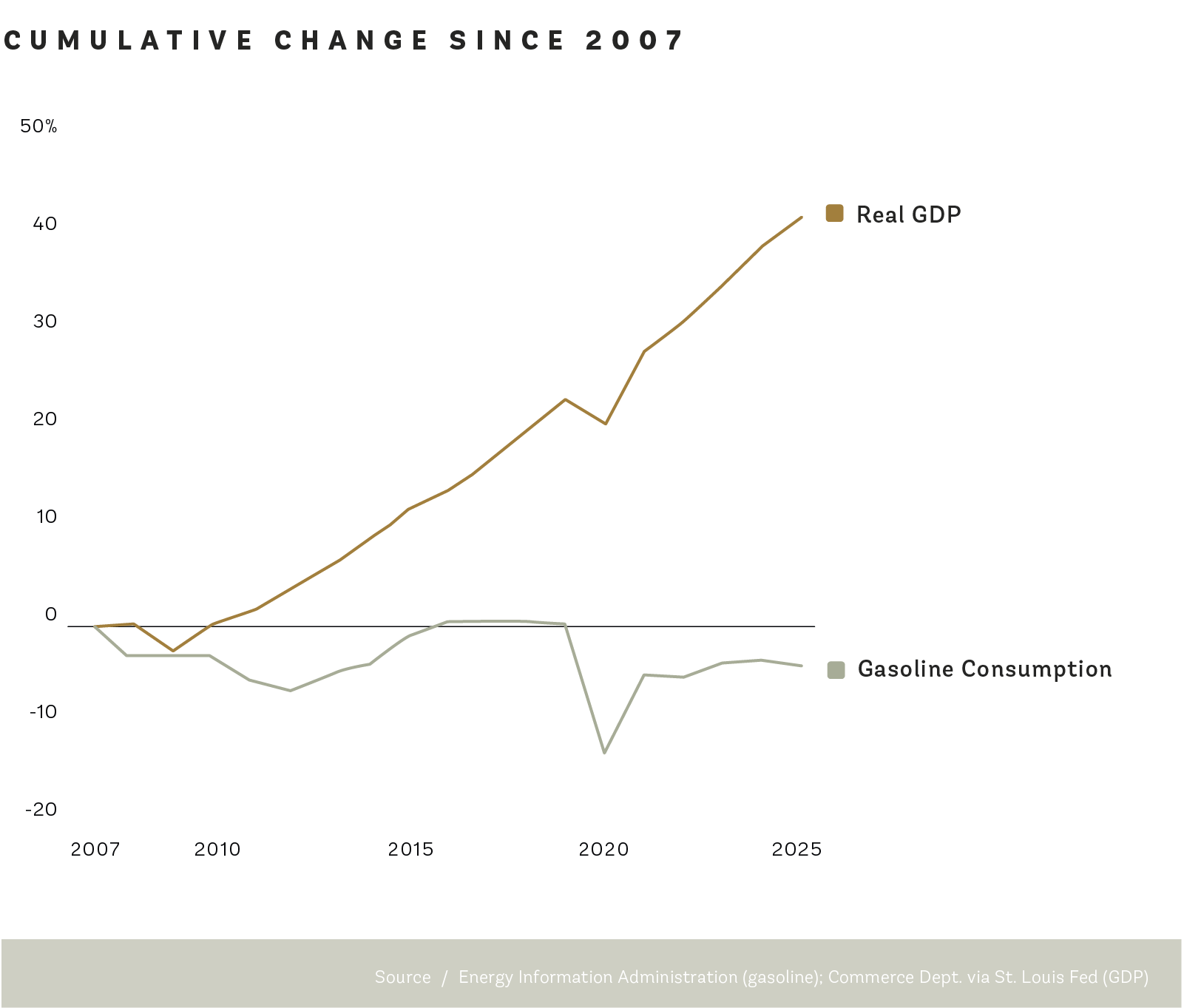

Even so, it is important to recognize that the U.S. economy is less vulnerable to rising energy prices than it once was. Higher oil prices can still act like a tax on households by raising gasoline and utility costs, which can in turn pressure consumption and add to inflation. But that effect has diminished as the economy has become less energy-dependent. Americans consumed about 4% less gasoline in 2025 than they did in 2007, even as real GDP grew roughly 42% over that same period. Energy’s share of household consumption has also fallen, from 5.7% in 2007 to 3.7% last year[i].

Even the sharp oil spike following Russia’s invasion of Ukraine in 2022 had a relatively modest macroeconomic effect. According to Federal Reserve research, it trimmed U.S. growth by just 0.13% while adding about half a percentage point to inflation. When you adjust for inflation at $100 a barrel today, the 2022 Russia invasion pushed the price of oil to $143 per barrel[ii]. The economy continued to grow.

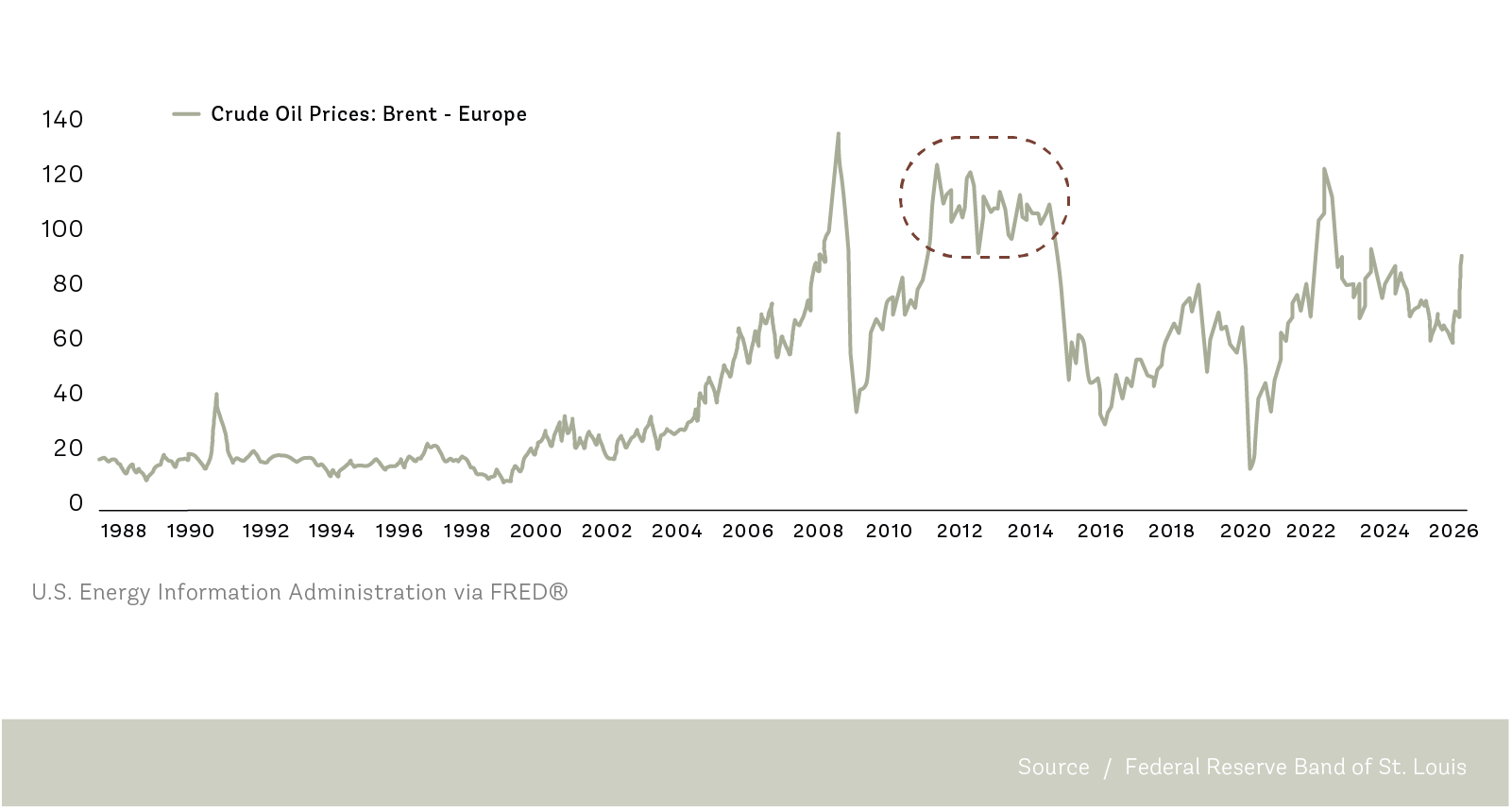

There was also a period from 2011 to 2014 when brent crude traded above $110 per barrel (chart below), which is a period that coincided with ongoing global economic expansion and rising equity markets.

The point is not that oil no longer matters, it certainly does. But it generally takes more than a temporary spike in energy prices to materially derail the U.S. economy. That is especially true when the broader economy is still showing signs of underlying resilience.

And that’s what we’re seeing as of this moment. The U.S. services sector (as measured by the ISM services index) rose to 56.1 in February, its highest reading since mid-2022. New orders climbed to 58.6, 14 of 18 service industries reported growth, and export orders also improved. These numbers suggest business activity is still expanding broadly.

Credit trends also look very strong. Across the developed world, loan growth is accelerating, with banks in the U.S., U.K., Eurozone, and Japan lending at the fastest pace seen in several years. I think this trend could hold for some time, given that yield curves across major developed markets are upward sloping. Banks can borrow at lower short-term rates and lend at higher long-term rates with attractive spreads. In the U.S., companies are also finding ample financing in bond markets, with investment-grade issuance topping $208 billion in January, one of the few times monthly borrowing has ever exceeded $200 billion[iii].

Taken together, these are not the kinds of conditions that typically accompany an economy on the verge of being knocked off course. We don’t think that means risks should be dismissed, but we do think it reinforces the importance of staying disciplined rather than reacting emotionally to uncertainty.

Conclusion

The International Energy Agency’s decision this week to coordinate the release of 400 million barrels of strategic reserves (the largest such action in its history) is another reminder that policymakers are not standing still as events unfold. While that move alone does not eliminate the risk of further volatility in oil and equity markets, it does underscore that there are some mechanisms in place to help cushion the blow if supply disruptions persist.

We understand these periods can be deeply unsettling for investors. Volatility is uncomfortable, uncertainty is unnerving, and when the headlines involve war, energy markets, and the possibility of broader economic fallout, it is entirely understandable that many people feel anxious and tempted to act.

That is precisely why moments like this call for added discipline. As Devin Moran wrote in his August 2024 piece, Planning for Market Volatility, “the issue that often troubles many investors—and ultimately hurts them—is that volatility increases the temptation to “time the market,” allowing short-term uncertainties to drive decisions that can have serious long-term consequences.”

We do not want to do that here.

That does not mean ignoring risk or deeming the situation insignificant. It means recognizing that financial markets ultimately respond to economic fundamentals like corporate earnings, productivity, capital investment, and long-term growth.

Sources:

[i] “Why the Oil Shock Probably Won’t Derail the Economy. And One Way It Might,” The Wall Street Journal, March 8, 2026.

[ii] “Why the Oil Shock Probably Won’t Derail the Economy. And One Way It Might,” The Wall Street Journal, March 8, 2026.

[iii] “US High-Grade Bond Sales Top $200 Billion in Record Yearly Start,” Bloomberg, January 29, 2026.

____________

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. This material was produced for Judy Rubino’s use. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.