Investing Through Technological Change

Over the past several weeks, we have received several inquiries from clients and friends asking variations of the same question:

Is Artificial Intelligence (AI) creating a bubble?

Is this new technology going to replace jobs and destabilize markets, or perhaps even upend the broader economy as we know it?

These are all, of course, rational questions given how quickly and profoundly AI is being developed and implemented. The tone surrounding the technology is markedly different from previous technological innovations like the internet and the iPhone. Instead of seeing technology as a productivity enhancer that could open new doors, AI is raising questions about replacing knowledge work altogether.

Many of you are thinking not just about your portfolios, but about your children, your grandchildren, and what the next decade might look like.

To make matters even more complex, very recent headlines have amplified concerns for many. Anthropic’s latest update to its Claude product contributed to a selloff in select software stocks, as it became apparent that AI could create workflows, execute them, and develop software needed to run them. A short time later, a widely circulated piece by Citrini Research outlined a fictional 2028 scenario in which AI-driven job losses spiral into recession, mortgage stress, and financial instability. The article was dramatic, detailed, widely shared, and led to market selloff (though stocks recovered the next day).

If you’re concerned, we hear you. And we empathize with the way uncertainty around this profound new technology can make many of you feel.

But when we step back from the narrative and examine the data we have in front of us, the current environment looks more measured than the headlines suggest.

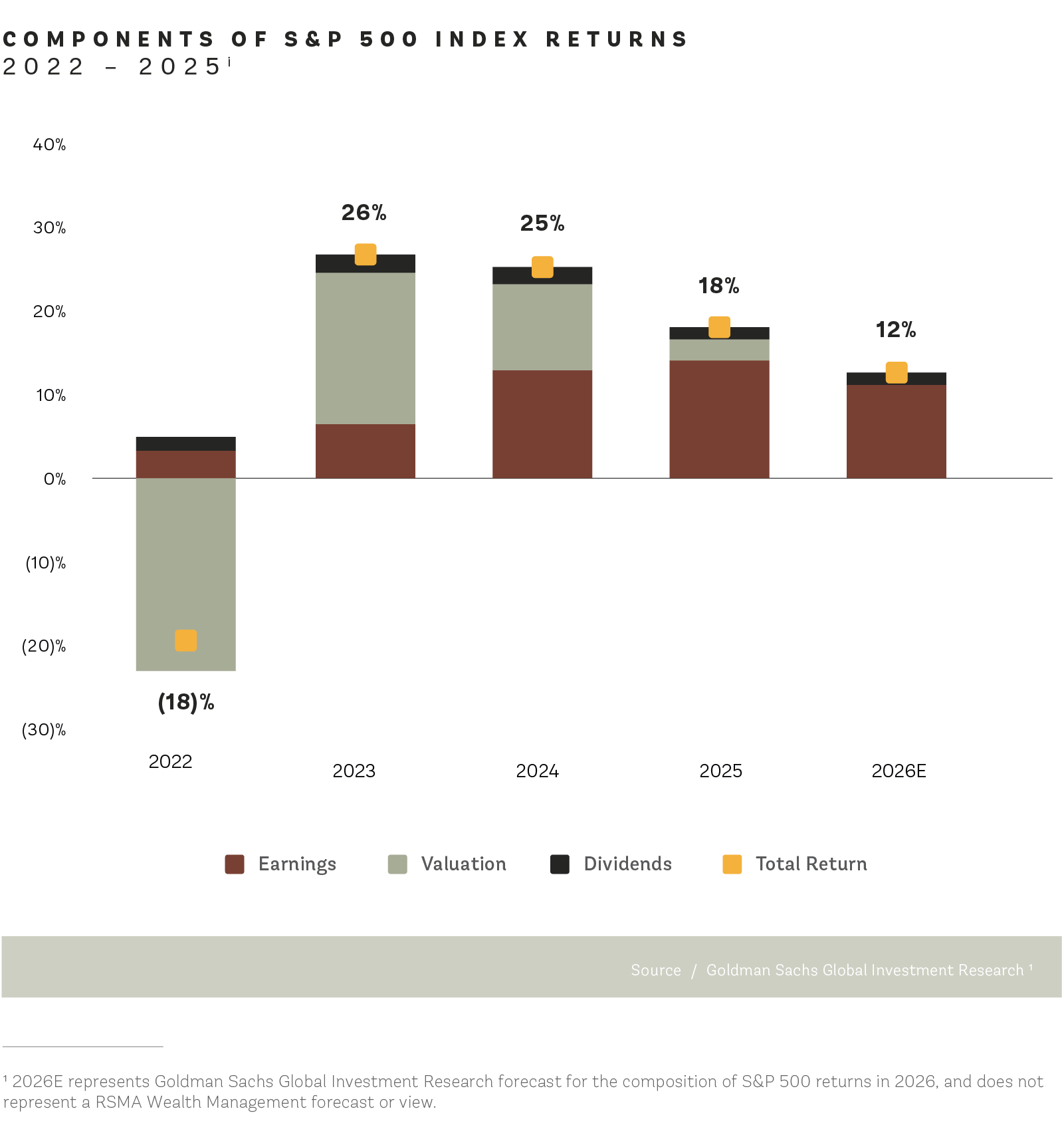

Let’s start with the “AI bubble.” As we wrote in our January letter, the idea that stock market gains are being driven purely by speculative excess simply does not match the numbers. A large portion of the S&P 500’s gains over the past couple of years has been supported by earnings growth, not runaway valuations. This is demonstrated by the red bars (earnings’ contribution to total S&P 500 returns) in the 2024 and 2025 portions of the chart below. This stands in sharp contrast to periods like the late 1990s, when valuations detached meaningfully from fundamentals.

According to Goldman Sachs, the 10 largest stocks in the S&P 500 (many of which are at the center of the AI theme) trade at valuation multiples roughly in line with their five-year averages and well below the extremes seen during prior bubbles. These companies also carry above-average earnings growth and profit margins.

The bigger concern on many investors’ minds is economic. Is AI going to hollow out white-collar employment? Will it trigger a wave of job losses that cascades into falling incomes, weaker consumer spending, and ultimately a broader recession?

These are valid, serious questions. But attempting to answer them requires something inherently dangerous for investors: trying to predict what the economy will look like several years into the future. The recent Citrini Research piece gained attention precisely because it painted a vivid picture of 2028, complete with unemployment spikes, mortgage stress, and systemic financial consequences. For anyone who wants to believe that AI will replace most human workers, it was the ultimate confirmation bias piece. But for observers who recognize that it was a forecast about structural economic transformation years in advance, the piece was more accurately viewed as pure speculation. As investors, we cannot position portfolios based on multi-year hypotheticals unsupported by current evidence.

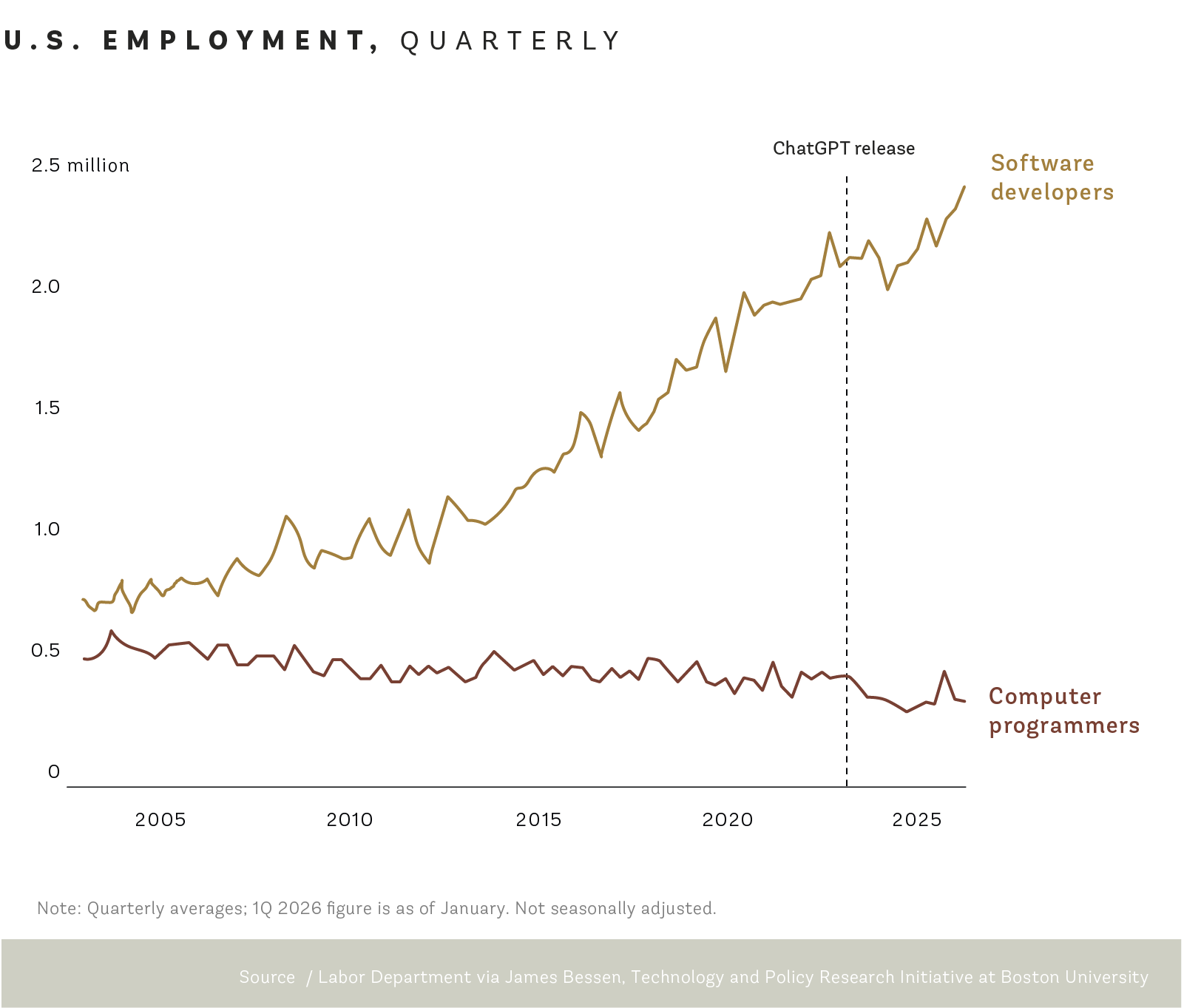

If the ‘jobs apocalypse’ were truly imminent, we should expect to see at least an inkling of evidence in labor markets statistics. But so far, it is not there. Software developers, for example, which is a profession widely viewed as among the most AI-exposed, have actually seen employment trend higher since the release of ChatGPT in late 2022. Anecdotally but importantly, young computer science graduates continue to earn substantial premiums relative to peers in other fields.

This pattern aligns with how technological change has historically unfolded. Technological advances almost always displace certain roles. But they also tend to do three things:

Increase productivity for remaining workers

Create new categories of employment

Lower costs, which boosts real purchasing power and supports demand elsewhere in the economy—leading to more jobs

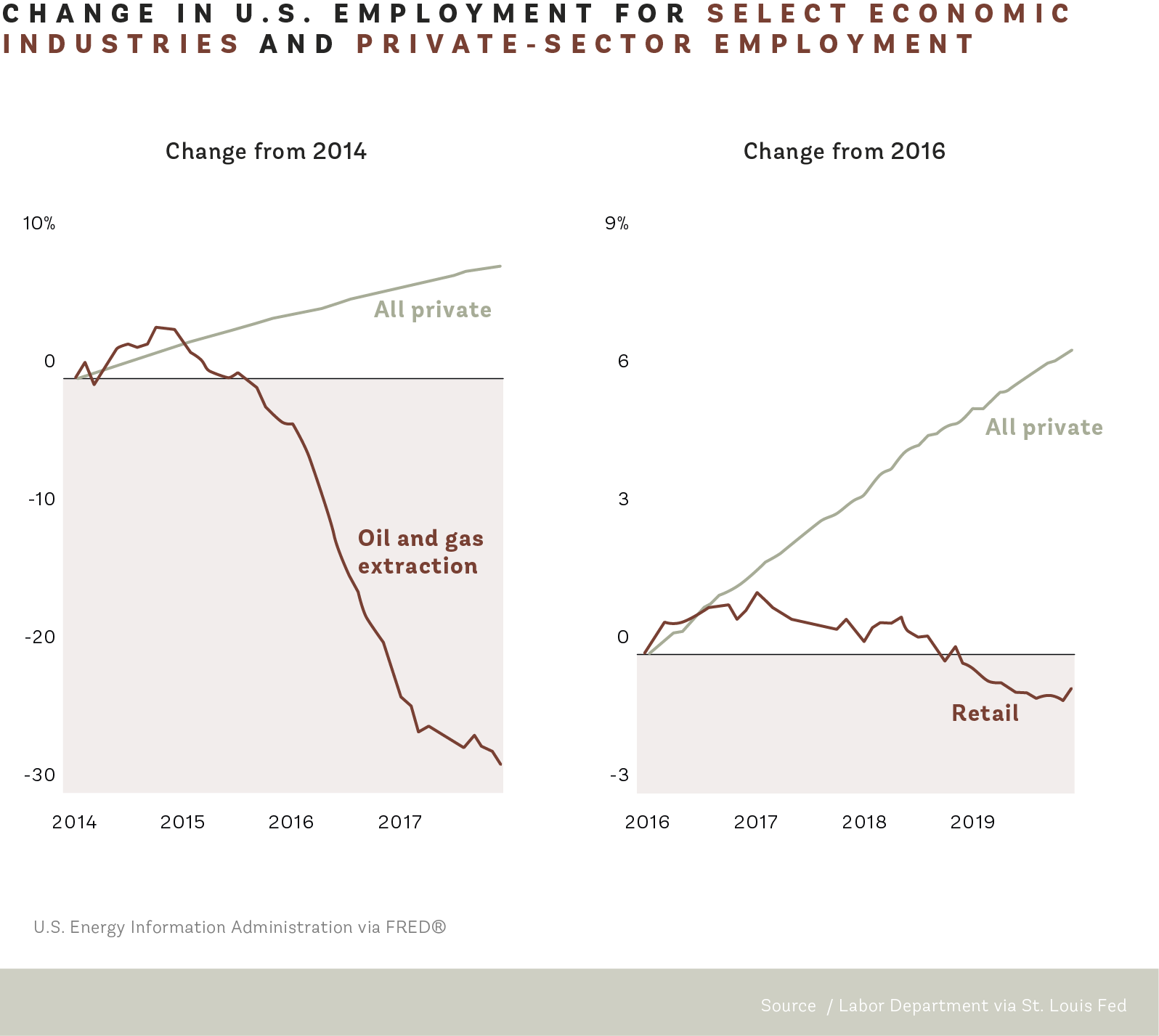

We have seen this dynamic repeatedly throughout history. Textile automation reduced agricultural employment but expanded manufacturing. ATMs reduced certain bank teller tasks, but total banking employment rose as branch networks expanded. Spreadsheet software reduced bookkeeping roles, but increased demand for financial analysts and accountants. Even after China’s entry into the WTO led to manufacturing job losses, overall U.S. employment continued to grow.

What We Are Watching From Here

Even as we offer a balanced view of how the economy may be impacted by this transformational technology, it would be imprudent to assume the adjustment process will be seamless. Rapid productivity shifts can create real dislocations before new equilibrium forms, and certain industries are likely to feel pressure more intensely and more quickly than others. Labor markets in specific categories could experience volatility over the short to medium term.

One area to watch is the scale of AI-related capital spending relative to underlying revenue growth. Periods of technological transformation can invite overinvestment. The late-1990s internet cycle is a useful reminder that infrastructure buildouts can temporarily exceed sustainable demand. Today’s AI investment wave is significant, and over time it will need to be justified by durable earnings.

A second factor to watch is the interaction between AI-driven efficiency and the broader economic cycle. If a recession were to begin for unrelated reasons, companies might accelerate automation and cost-cutting initiatives already under consideration. That could amplify job losses within certain segments, even if the broader labor market remains resilient.

The upshot is that these risks are measurable. They would show up in earnings revisions, capital spending data, hiring trends, and credit conditions long before a systemic breakdown became visible. For now, the evidence points to adjustment and investment, not a widespread economic fracture. Corporate profits remain the primary driver of market gains, and labor data in highly exposed sectors has not deteriorated in a way that confirms more extreme scenarios.

Our responsibility is not to dismiss uncertainty, nor to anchor portfolios to long-range forecasts built on hypothetical outcomes. It is to monitor conditions as they evolve, maintain diversification, and adjust positioning when the data changes.

____________

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. This material was produced for Kari Skedsvold’s use. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

Investing involves risk including loss of principal. No strategy assures success or protects against loss.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.