Year-End Tax Planning and Looking Ahead to 2026

First, we want to thank everyone for placing their trust in RSMA Wealth Management over the past year. We value our relationship with you, and as always, we thank you for being clients.

There was no shortage of ups and downs in 2025, and uncertainty ran high for much of the year. But in our view, the best way to see through the fog is to stick to the long-term plans we’ve put in place for you, adjusting them along the way as your objectives and financial situation change.

We’ll continue this work in 2026.

With just a couple of weeks left in the year and significant changes to the tax code coming in 2026, we’re focusing our year-end letter on the key highlights to be aware of as you plan ahead.

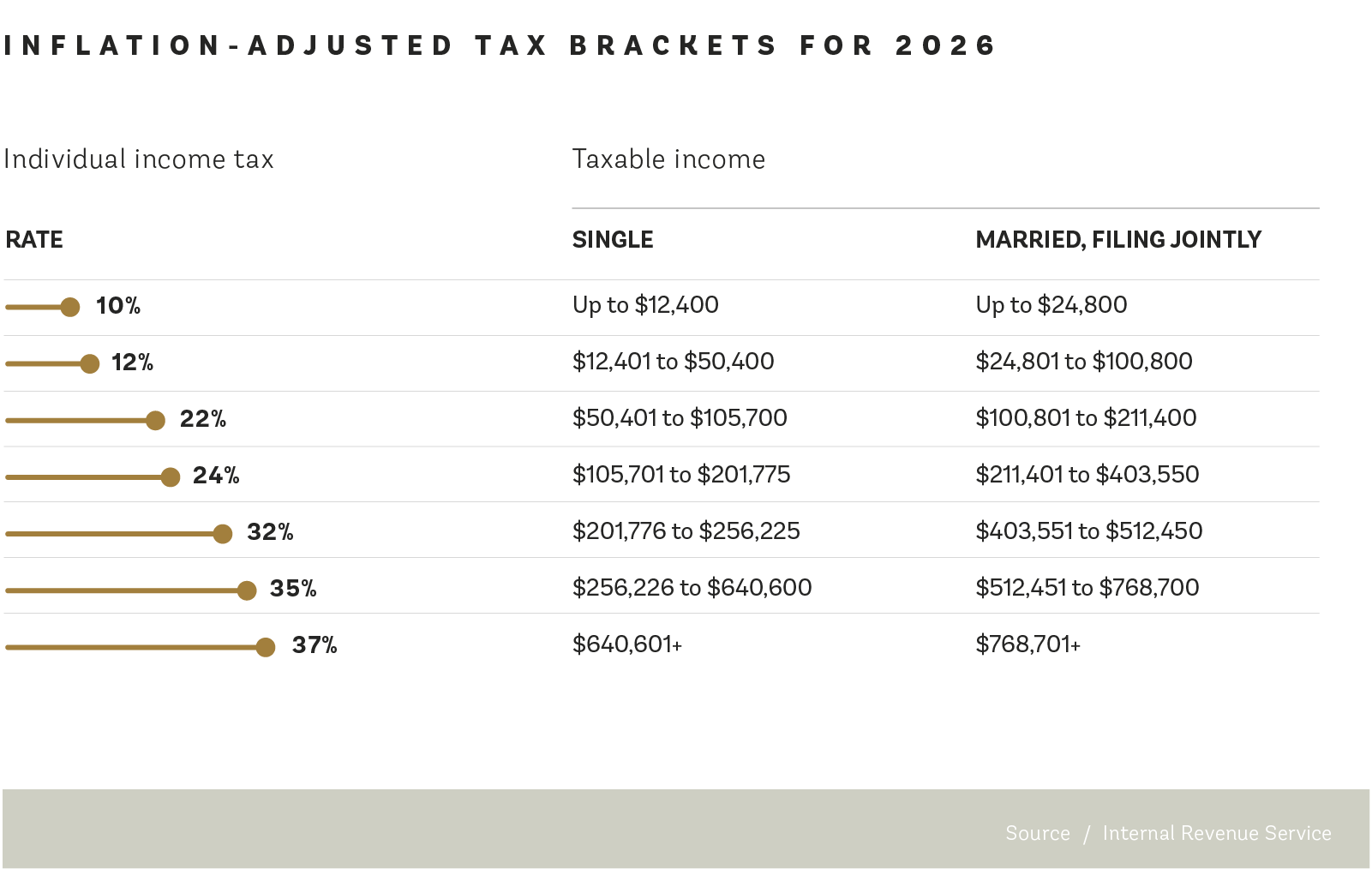

1.

Updated Tax Brackets for Next Year

2.

A Few Tax Moves to Consider Before Year-End

Qualified Charitable Distributions

For retirees who are charitably inclined, Qualified Charitable Distributions (QCDs) remain one of the most effective ways to give, in our view. Unlike traditional charitable donations, these transfers reduce your taxable IRA income directly, which can help manage AGI-related thresholds such as Medicare premium surcharges.

Key Items to Know[i]:

$108,000 – Individuals age 70½ or older can direct up to $108,000 from an IRA to qualifying charities in 2025, and couples with two IRAs can each make their own gifts.

Direct Transfer – For a distribution to qualify, the funds must move straight from the IRA to the charity. The donor cannot take possession of the money first

Withdrawal Sequence Matters –The IRS generally counts the first dollars withdrawn from an IRA as part of that year’s required minimum distribution (RMD), if an RMD applies. That means if you take your full RMD early in the year and only later attempt a QCD, the charitable transfer will not offset any portion of the RMD—it will simply be an additional distribution. To ensure the QCD counts toward the RMD, many specialists suggest completing QCDs before taking other withdrawals.

December 31 Deadline -- the donation generally must be cleared by December 31 to be reflected properly for the tax year.

Documentation – As with all charitable contributions of $250 or more, donors must obtain a written acknowledgement from the receiving organization before filing their tax return. The letter must confirm the gift amount and that no goods or services were received in exchange.

Thinking About State and Local Tax Timing

The new tax law increases the cap on state and local tax (SALT) deductions to $40,000 for 2025, with a scheduled increase to $40,400 in 2026 and a gradual 1% annual rise through 2029[ii].

In some cases, making additional payments before December 31 can improve your deduction, but in others it may not. Because the interaction with alternative minimum tax and other phaseouts can be complex, this is an area where running the numbers with a CPA is particularly important.

3.

Tax Planning Considerations for Retirees and Seniors

For retirees, tax decisions often intersect with income needs, Medicare costs, and legacy goals. Here are a few themes to keep in mind.

Taking Advantage of New Senior-Focused Deductions

Beginning in 2025, taxpayers age 65 and older are eligible for an additional “senior” deduction on top of the standard deduction—$6,000 for single filers and $12,000 for married couples filing jointly—subject to income limits.

The benefit phases out above $75,000 of income for single filers and $150,000 for joint filers and is scheduled to be available through 2028[iii].

There are also provisions that provide relief on the taxation of Social Security benefits for those over 65 from 2025 through 2028, although detailed IRS guidance on how these rules will operate is still pending.

These changes reinforce the importance of looking at retirement income sources—pensions, IRA withdrawals, brokerage income, and Social Security—together rather than in isolation.

Coordinating with Estate and Gifting Strategies

The federal estate and gift tax exemption rises to $15 million per person in 2026, with the annual gift exclusion at $19,000 per recipient[iv].

For families with significant assets, this higher lifetime exemption opens a window to move appreciating assets into trusts or to make larger gifts to the next generation without incurring estate or gift tax.

These decisions are highly individualized, but the combination of higher thresholds and generous annual exclusions gives retirees considerable flexibility.

Managing Required Minimum Distributions and QCDs

Under prior legislation, required minimum distributions now begin at age 73, with a scheduled increase to age 75 later in the next decade[v]. Those distributions are generally taxable, but as noted above, QCDs offer a way to satisfy part or all of an RMD while keeping the distributed amount out of adjusted gross income (AGI).

As we wrote above, because the first dollars out of an IRA typically count toward the RMD, it’s important to arrange QCDs before taking other withdrawals if you want them to apply to that year’s requirement. Done properly, QCDs can help support the causes you care about and reduce the risk of crossing income thresholds that trigger higher Medicare premiums or other surcharges.

4.

Tax Planning Ideas for Working Individuals and Families

For those still in their working years, year-end is an opportunity to check that you’re making full use of the tools available to you—and to prepare for rule changes coming in 2026.

Retirement Plans and HSAs

For 2025, employees can contribute up to $23,500 to a 401(k) plan, with an additional $7,500 catch-up contribution available from age 50 onward.

Workers aged 60 to 63 have access to a larger “super catch-up” of $11,250.

Here are the max deferrals for 2026:

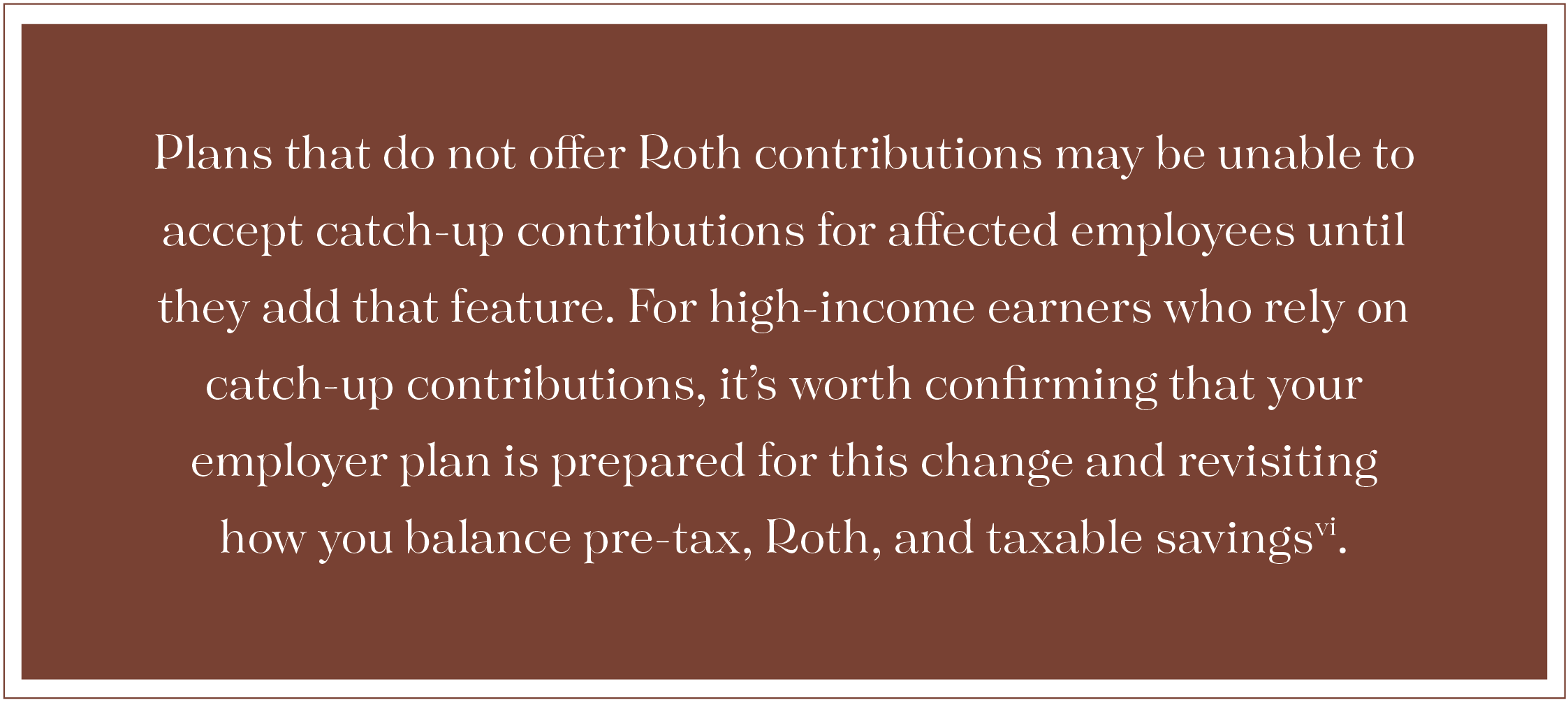

Upcoming Roth-Only Catch-Ups for Higher Earners

We’ve been hearing quite a few questions about this provision. Here’s how it works.

Beginning in 2026, employees whose prior-year wages exceed $145,000 (indexed for inflation) will generally be required to make 401(k) catch-up contributions on a Roth basis rather than pre-tax, provided their plan offers a Roth option.

This change effectively shifts tax on those catch-up dollars into the current year, but allows the funds to grow and be withdrawn tax-free in retirement if the usual Roth rules are met.

Deductions and Credits in 2026

The standard deduction is scheduled to increase to $16,100 for single filers and $32,200 for married couples filing jointly, and the income thresholds for each tax bracket (as shown in the table above) will shift upward as well, meaning that a similar level of income may fall into slightly lower effective tax.

The $2,200 child tax credit continues[vii].

In Closing

Because tax decisions depend heavily on your individual situation, we encourage you to coordinate with your CPA and reach out to us if you’d like to explore any of these ideas in more detail.

If you’re considering larger charitable gifts, evaluating Roth versus pre-tax savings, thinking about gifts to children or grandchildren, or anticipating a year with unusually high income, please let us know how we can help you plan.

Thank you again for being a client. We wish you a healthy and happy holiday season and New Year.

Sources:

[i] “How the Megabill Boosts a Charitable Tax Break for Seniors,” September 5, 2025, The Wall Street Journal.

[ii] “The 2026 Tax Brackets are Here. See Where You Land,” October 9, 2025, The Wall Street Journal.

[iii] “2025 Tax Deductions for Those Over Age 65,” Kiplinger.

[iv] “The 2026 Tax Brackets are Here. See Where You Land,” October 9, 2025, The Wall Street Journal.

[v] “How the Megabill Boosts a Charitable Tax Break for Seniors,” September 5, 2025, The Wall Street Journal.

[vi] “High Earners Age 50 and Older are About to Lose a Major 401(k) Tax Break,” September 24, 2025, The Wall Street Journal.

[vii] “The 2026 Tax Brackets are Here. See Where You Land,” October 9, 2025, The Wall Street Journal

____________

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change. All indices are unmanaged and may not be invested into directly. Past performance is no guarantee of future results.

Prior to investing in a 529 Plan, investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.